Resources

The Hidden Math of ROI: Thinking Beyond Labor Savings in Advanced Manufacturing

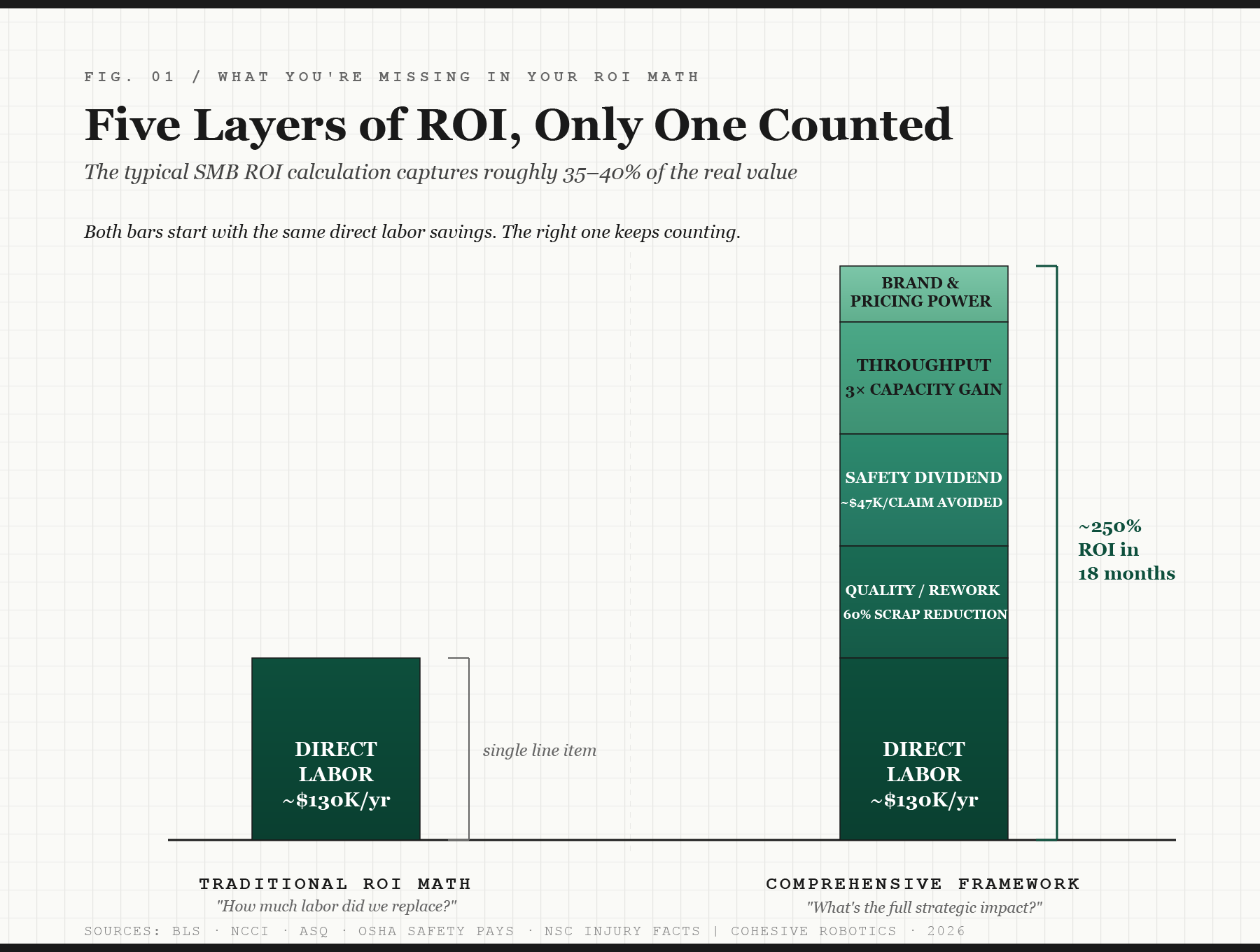

A serious manufacturing ROI framework in 2026 has to account for things beyond repurposing labor. There are four other layers that don't always show up on the standard ROI spreadsheet: quality, safety, throughput, and brand. Together, those layers routinely deliver more value than the labor line itself. This is the case for what we call the "Hidden ROI" — and why every manufacturing leader at SMBs evaluating a robotics investment needs to do the comprehensive math, not the convenient one.

June 17, 2026